.svg)

Shareholders can defer or eliminate capital gains taxes on their sale proceeds, while their businesses gain corporate tax deductions and can become income tax-free entities.

Partial sales are common, and transactions can be tailored to buy-out targeted shareholders. Employee-owned companies can also engage in future M&A deals.

Employee ownership enables firms to remain independent and rooted in their communities. Founders, family, and other shareholders can maintain equity and meaningful roles.

Employee ownership is not a handout. The benefits are meaningful, but the opportunities are earned.

Eligible staff are allocated stock over time, and those shares are subject to vesting. In the long run, employee owners gain skin in the game and wealth-building opportunities.

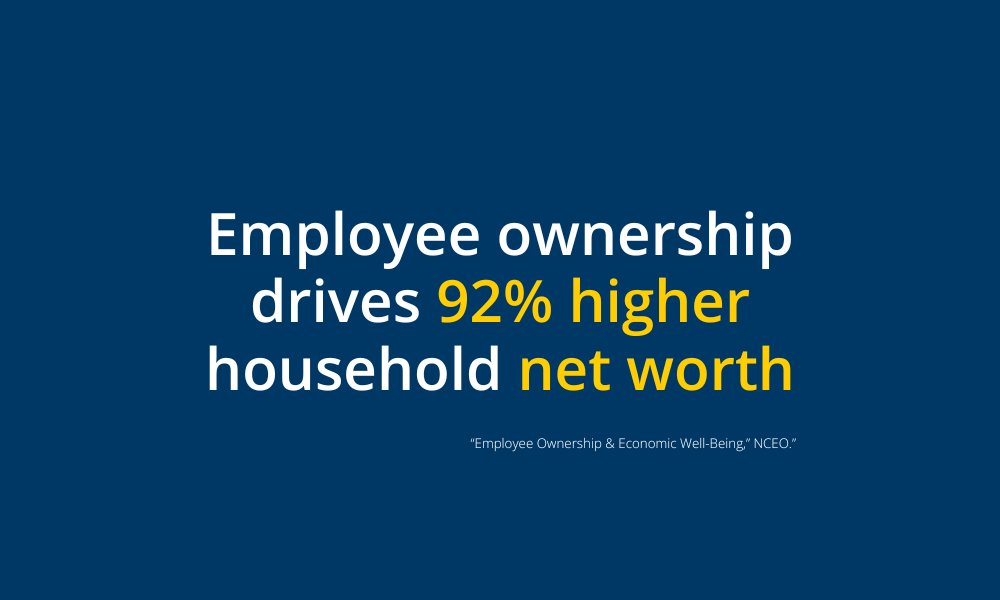

This helps foster "ownership cultures" that can propel businesses and their communities to new heights. Research has shown that employee owners and their firms outperform their peers in terms of business metrics and standards of living.

Need an ESOP refresher? Download our guide for a concise overview of the mechanics and benefits of employee stock ownership plans.